Celebrating 40 years of creative advertising, #39: MSGCU: Financial Champion.

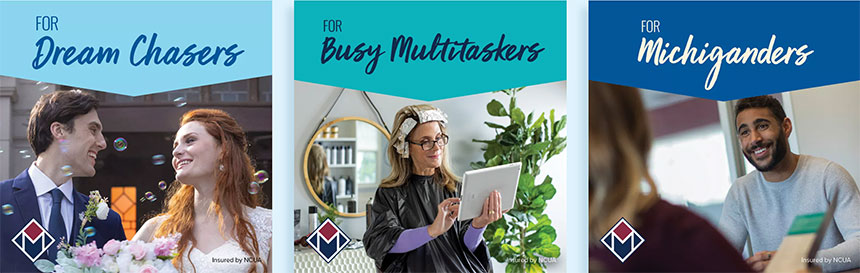

Because bank products can be so similar across the industry, many financial advertising campaigns fall back on promoting “friendly and helpful service”— even when this claim is not borne out by consumers’ experience. For Michigan Schools and Government Credit Union … Read article